The Howe, Thieu, Cheathem and Dew Problem. Joachim N. Walkout is the investment counselor at the How

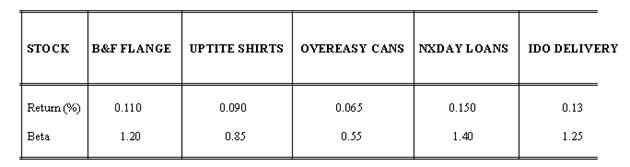

Question: The Howe, Thieu, Cheathem and Dew Problem. Joachim N. Walkout is the investment counselor at the Howe, Thieu, Cheathem and Dew Investment Company. Joachim is in the process of setting up an investment scheme for a group of impoverished distant learning operations research professors. Five stocks have been identified as having very favorable expectations for the near term. Although expected return is important, risk must also be considered. Typically risk is measured by the beta factor that is used in the capital asset pricing model developed by Nobel laureate William Sharp of Stanford. A beta of 1.00 means that a company is matching the risk of the entire market average. Beta values greater than 1.00 indicates that the stock has a relatively high risk. Beta values of less than 1.0 indicate stocks that are safer than the average of the market. The expected near term returns and the latest beta calculations for the five stocks that Joachim has identified are as follows:

Joachim would like to calculate what percentage should be devoted to each of the five stocks, that is, what percentage of the professor’s nest egg should be invested in which of the five stocks. The objective is to minimize risk while insuring at least an 11 percent return. They would also need to diversify. Therefore no more than 35 percent should go to any one stock. What percent should be devoted to which stocks?

Deliverable: Word Document

-

a. You are the manufacturer of two sizes of frammits, large and small. You have a machine that can s #704") (See Solution) a. You are the manufacturer of two sizes of frammits, large and small. You have a machine that can s #704

(See Solution) a. You are the manufacturer of two sizes of frammits, large and small. You have a machine that can s #704

-

[Solution] Project Evaluation. The following table presents sales forecasts for Golden Gelt Giftware. The unit #20301

-

[Solution] The Midtown Market purchases apples from a local grower. The apples are purchased on Monday at 2.00 #9216

-

(See Solution) Apiece of heavy equipment is two 8-foot metal arms that make a V with the horizontal plane and forms #24066

-

Math Solutions

-

Step-by-Step Math Solutions

a. You are the manufacturer of two sizes of frammits, large and small. You have a machine that can s #704")

Apiece of heavy equipment is two 8-foot metal arms that make a V with the horizontal plane and forms #24066")